Monopoly in Diamond Supply Gives Way to Oligopoly, Albeit With Healthy Market Forces

In what represents the longest monopoly in history, De Beers controlled the global diamond market for almost a century! Almost all of the world's rough diamonds used to be sold through the De Beers distribution channel, Central Selling Organisation or CSO (later changed to Diamond Trading Co. or DTC). CSO had the power to use its discretion to sell when and to whom it wanted. It had the muscle to hold on to inventory in a weak market or raise the prices charged to Sightholders. When prices were high enough to negatively affect demand, the company could release inventory and restrain further price rises.

In the second half of the 20th century, as more and more world class mines were discovered in Russia, Australia and Canada, it became increasingly difficult for De Beers to control all global supply. Over the last quarter of a century, a string of happenings led to the unravelling of the company's monopolistic hold of the market. Russia (currently the world's largest diamond producer by value) split its production from De Beers in the 1990s. The Argyle Mine in Australia and other mines followed suit, selling independently of De Beers.

In 2001, multiple lawsuits were filed in U.S. courts alleging that De Beers “unlawfully monopolized the supply of diamonds, conspired to fix, raise, and control diamond prices, and issued false and misleading advertising.” De Beer’s monopolistic reign had officially ended. After several appeals, in 2012 the U.S. Supreme Court denied review of final petition and there was a settlement to the tune of $295 million with an agreement to “refrain from engaging in certain conduct that violates federal and state antitrust laws”.

Today, the diamond industry shows every sign of a typically oligopolistic market. The two largest players in the industry enjoy a strong market share of 62.5% as well as the power to set selling prices for their diamonds. The third, fourth and fifth largest players together enjoy 20.2% of market share. This block however, follows market-dictated means to fix prices. Although De Beers still enjoys a large share of the rough diamond supply market, the emergence of other big players has ensured that market forces drive the sector and prices much more than they did in the past.

In both a monopolistic as well as an oligopolistic system, it is a seller’s market. Although there are several mines today, the power of price leverage comes from having a considerable stake in supply relative to the industry as a whole. Although most diamond mines have more than one owner, typically only one entity manages operations, including diamond sales.

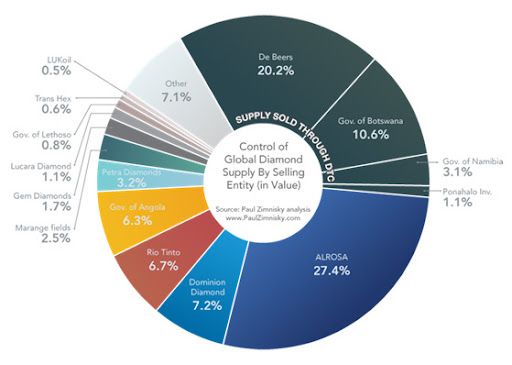

Chart showing estimated control of global rough diamond supply by selling entity.

DTC is the selling entity for De Beers and its partners (35% share of global rough diamond selling).

All figures are based on the estimated total value of diamonds held by selling entity from ROM.

Source: Paul Zimnisky

DTC does enjoy pricing power because overall, it controls the selling of an estimated 35% of global diamond production. It sells a large majority of its diamonds to a pre-selected group of buyers referred to as Sightholders at 10 organised sales a year (Sights), on a set-price, take-it-or-leave-it basis. In spite of the price rigidity, Sightholders are loyal because they perceive the quality and even the quantity of diamonds offered as unparalleled.

For DTC, a reliable diamond supply means a retention of its customers, which in turn translates to pricing power for De Beers. De Beers adjusts the supply offered through DTC to match demand, which has afforded De Beers the ability to keep their offering prices very stable, although with moderate upward movement. Of course, DTC also sells for the Government of Botswana, Namibia and Ponahalo Inv.

ALROSA is said to sell 50-70% of its domestic production through long-term contracts that work in a similar way as the Sightholder system. The remainder is sold through auctions, other bidding systems, and one-time contracts. ALROSA sets the price of the diamonds that it sells via long-term contract, and its buyers are steadfast, again because supply is reliable and of high quality.

Besides De Beers and ALROSA, there are 6 other entities that control the selling of at least 1% or more of global diamond supply. Most of them sell their diamonds by means of tenders, auctions, and spot sales. Rough diamond supply sold by tenders, auctions, and spot sales tend to reflect the actual market value for rough diamonds, and thus these prices influence De Beers and ALROSA when they set prices for Sights and long-term contracts.

With supply of diamonds being dominated by only a small number of firms, and this unlikely to ever change because of limited resource availability, exclusive resource ownership and high barriers to entry, there’s no denying that the diamond industry has the characteristics of an oligopolistic market. But, oligopoly or not, today, suppliers, buyers and consumers, all seem to be very comfortable with the system. The first rung of suppliers exhibit final control on their own prices, and mostly sell high-quality produce to regular buyers; the second rung definitely exhibit an extent of influence on prices at large because they too do have a sizeable share of the market; there is more of a spread of buyers than there were in the days of De Beers’ monopolistic control, so everyone has access to inventory; and end-consumers don’t seem to mind high prices at all because that’s what retains the exclusivity of a product they love to flaunt.